Solo founders are 63% of new startups in 2026 (Stripe)

The best solo founders in 2026 do not look like lone hackers compensating for the absence of a co-founder.

They look like the natural owners of a new company shape: AI-native, usually B2B, global from day one, built around recurring revenue, and unusually close to the customer.

Stripe's latest analysis puts numbers behind that shift: 63% of all new C corps formed through Stripe Atlas in Q2 2026 were solo-founded.

Source: Stripe Atlas

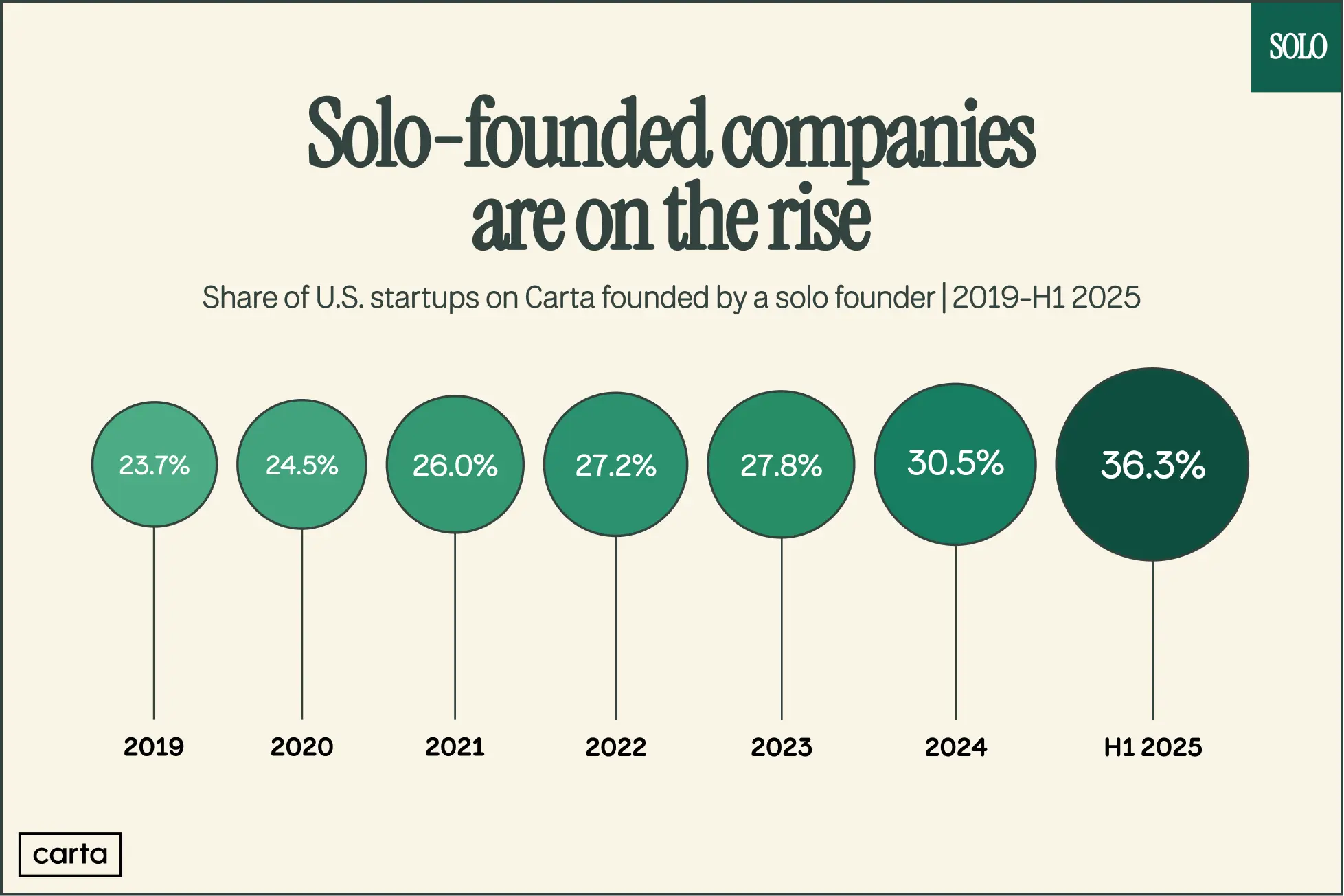

That number is directionally aligned with our Solo Founders Annual Report, built on Carta's dataset of tens of thousands of companies: over a third of all new U.S. companies are now solo-founded, up 53% since 2019.

Source: Solo Founders Annual Report

Stripe and Carta are measuring different moments in the company lifecycle. Stripe Atlas sees founders at incorporation. Carta sees companies later, once equity and fundraising enter the picture.

That likely explains most of the gap. Many founders incorporate solo before deciding whether to add a co-founder. But both datasets point in the same direction: solo founding is rising.

Stripe's analysis goes beyond the headline stat. It identifies several traits that separate top-decile solo founders from the rest, and each one lines up with what we've been seeing in our work.

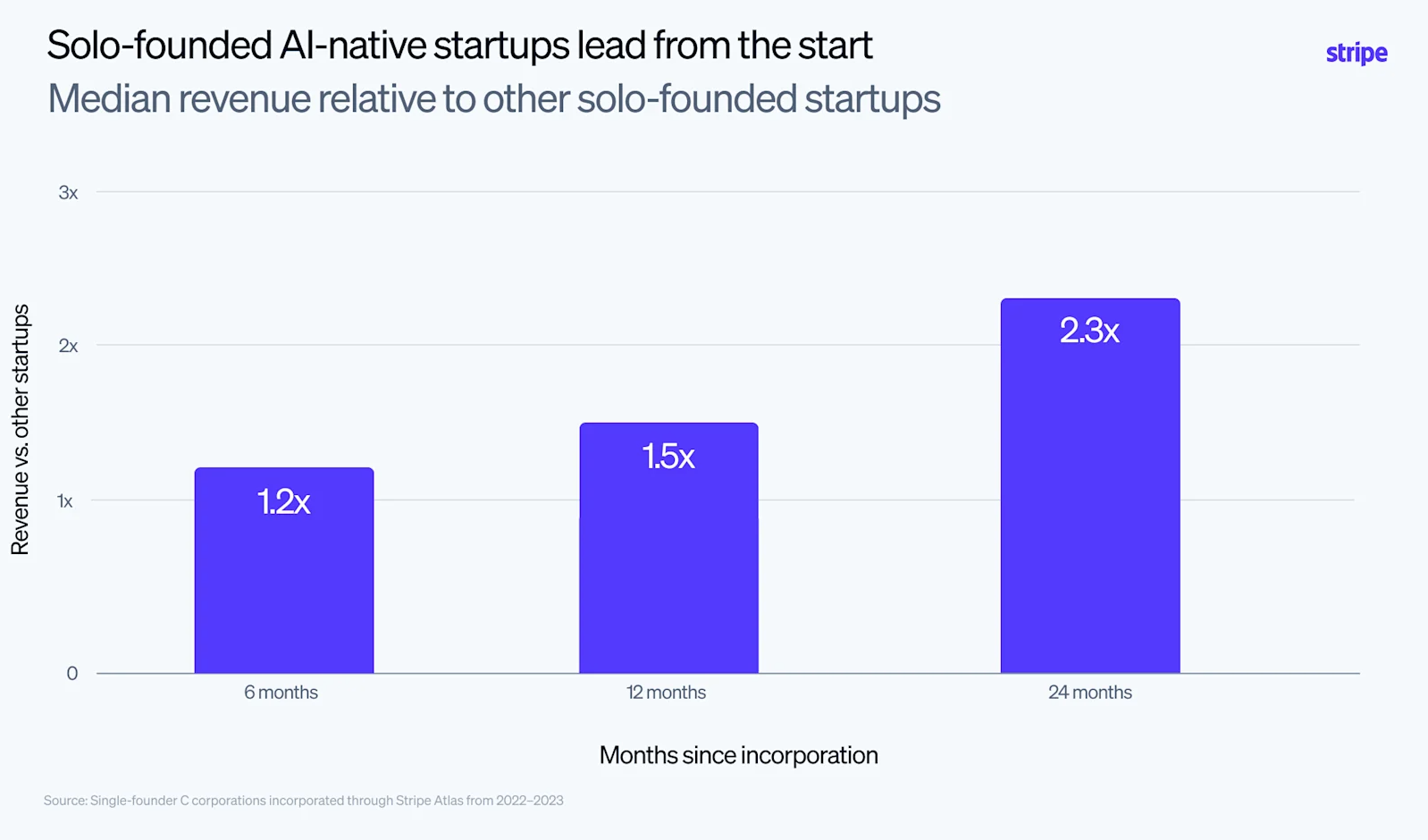

AI is the new co-founder

Solo-founded AI-native startups generated 2.3x the revenue by month 24 compared to other solo-founded startups.

This is what the fastest-growing solo founders we see are already doing.

Ben Cera, solo founder of Polsia, came on our podcast three months ago with $1.5M annualized revenue. He's since grown that to over $10M:

"If you have a new company and you don't make it 80% autonomous, meaning 80% of the operations and engineering and marketing day to day is not done by AI, you will be cooked. If it's a good idea, someone else will apply that, and they will beat you because they'll go faster, cheaper."

Earlier this week, Ben announced a $30M raise at a $250M valuation.

Another AI-native startup in the second cohort of the Solo Founders Program went from $0 to $2M ARR in four months.

Infrastructure, not lifestyle businesses

Stripe’s findings point to one company shape that shows up again and again among top-decile solo founders: B2B, sell globally, and bill on a recurring basis.

Two of our most-listened-to episodes this year are textbook examples:

Michael Grinich's WorkOS is the API platform that makes SaaS apps enterprise-ready. WorkOS customers include OpenAI, Anthropic, and Cursor, and the company was recently valued at $2B.

- Paul Klein IV's Browserbase is the headless browser infrastructure for AI agents, used by Microsoft, Clay, and Ramp.

These are not lifestyle businesses with a few customers. They are infrastructure companies: global, recurring, embedded, and built by founders who can use software and AI to cover more surface area than a small team could have a decade ago.

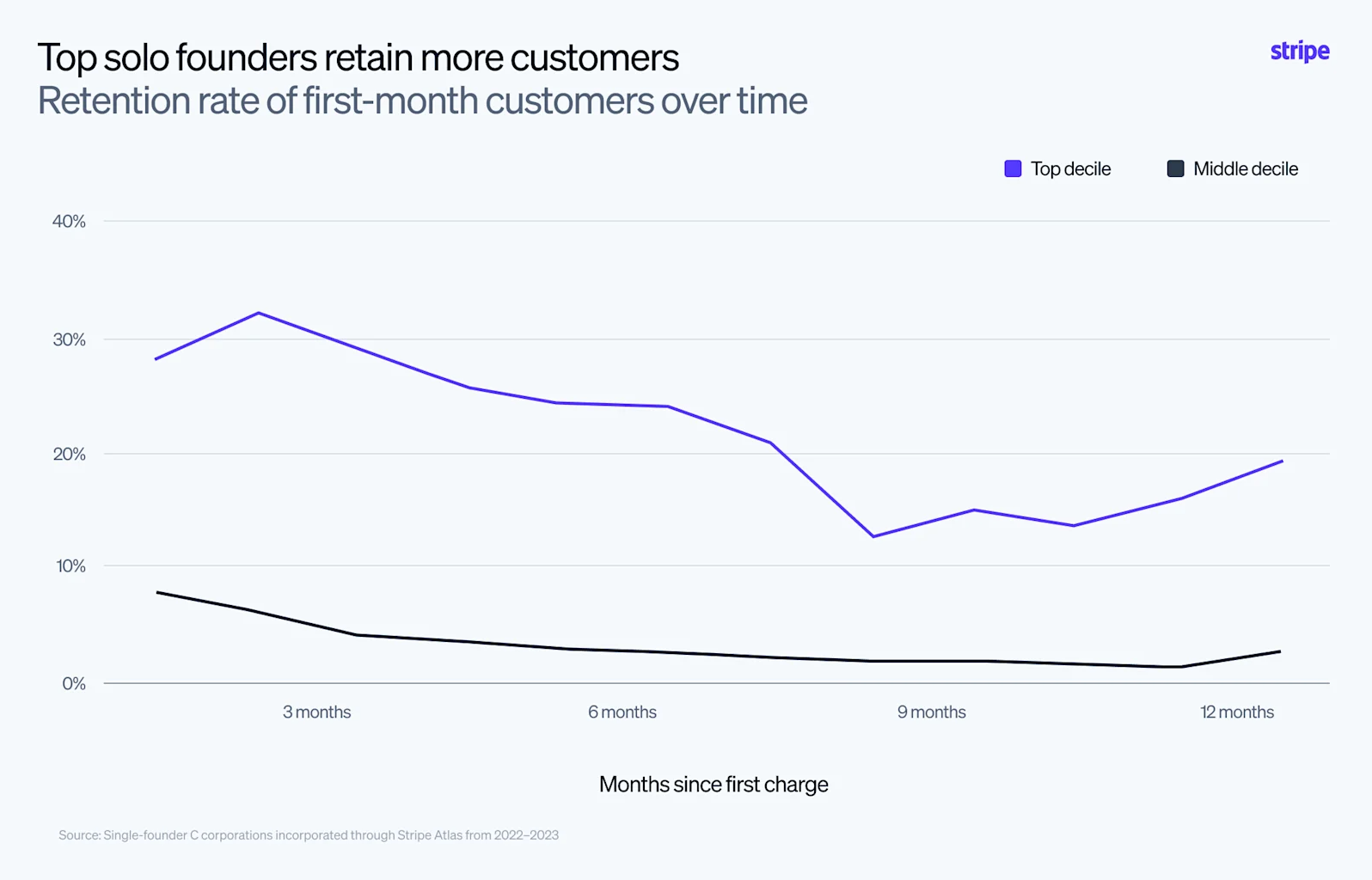

Be the bread guy

Month-2 customer retention is roughly 30% for top-decile solo founders vs. 8% for the median. Customers acquired in month one spend 47% more by year two at top startups.

In the early days, a solo founder is the salesperson, support rep, onboarding lead, and product team all at once. There's no translation layer between what customers say and what gets shipped.

We dug into this with Michael Grinich on last week's podcast:

"Our relationship with our customers today is much more like a partner. I'll be this durable supplier over a long period. You're a restaurant, and I'm your bread guy. I bring you bread every night at the same time, because if you're out of bread, your guests freak out."

That kind of relationship gets harder to preserve as customer context gets distributed across sales, support, product, and engineering. In the earliest days, solo founders often have the clearest possible line from customer pain to product change.

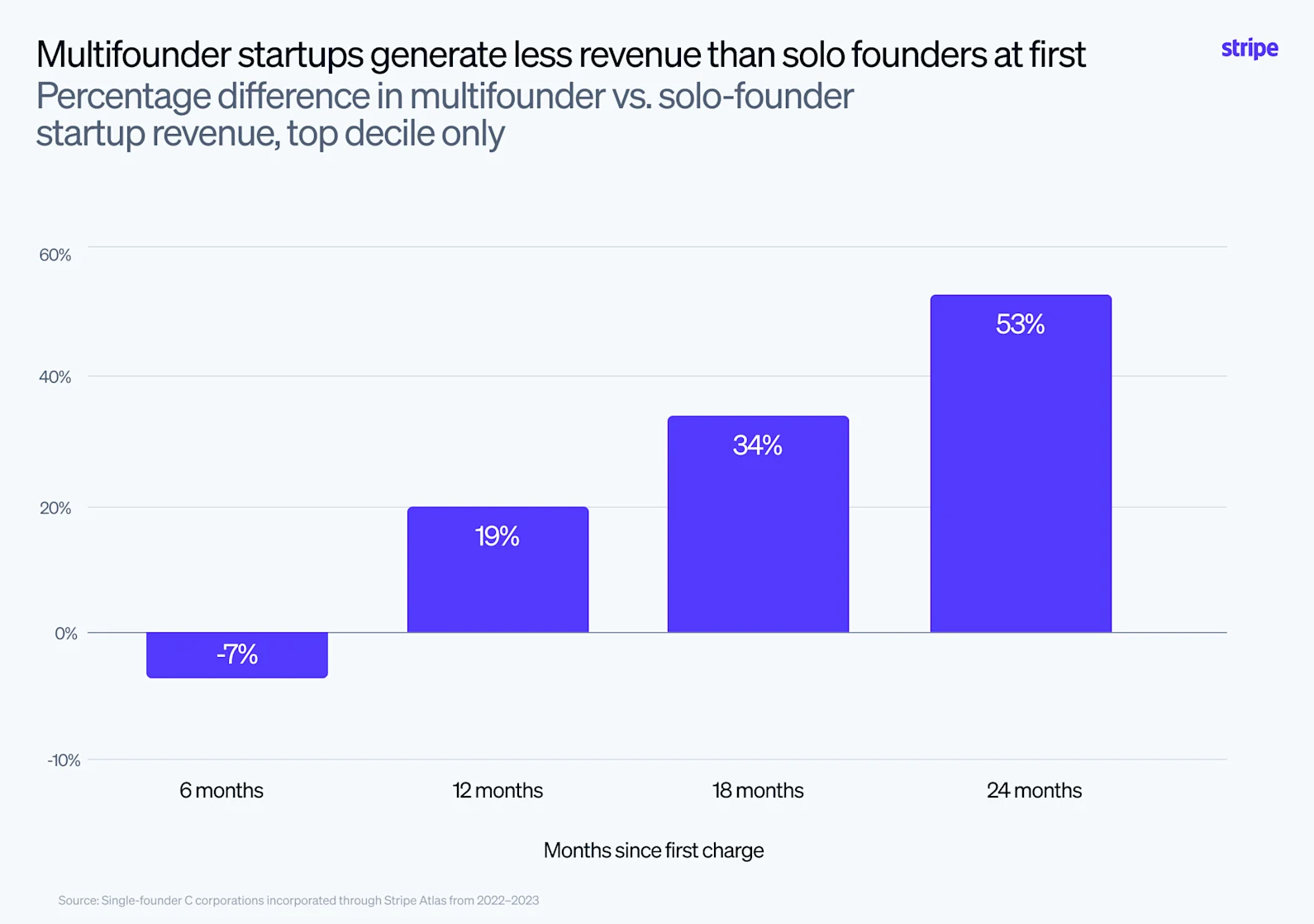

Comparable funding, more ownership

The Stripe finding most likely to get pulled out of context: top multi-founder teams generate 53% more revenue by month 24 than top solo founders.

But revenue at month 24 is not the same thing as company or founder outcomes.

First, solo founders raise comparable rounds at similar valuations to multi-founder teams.

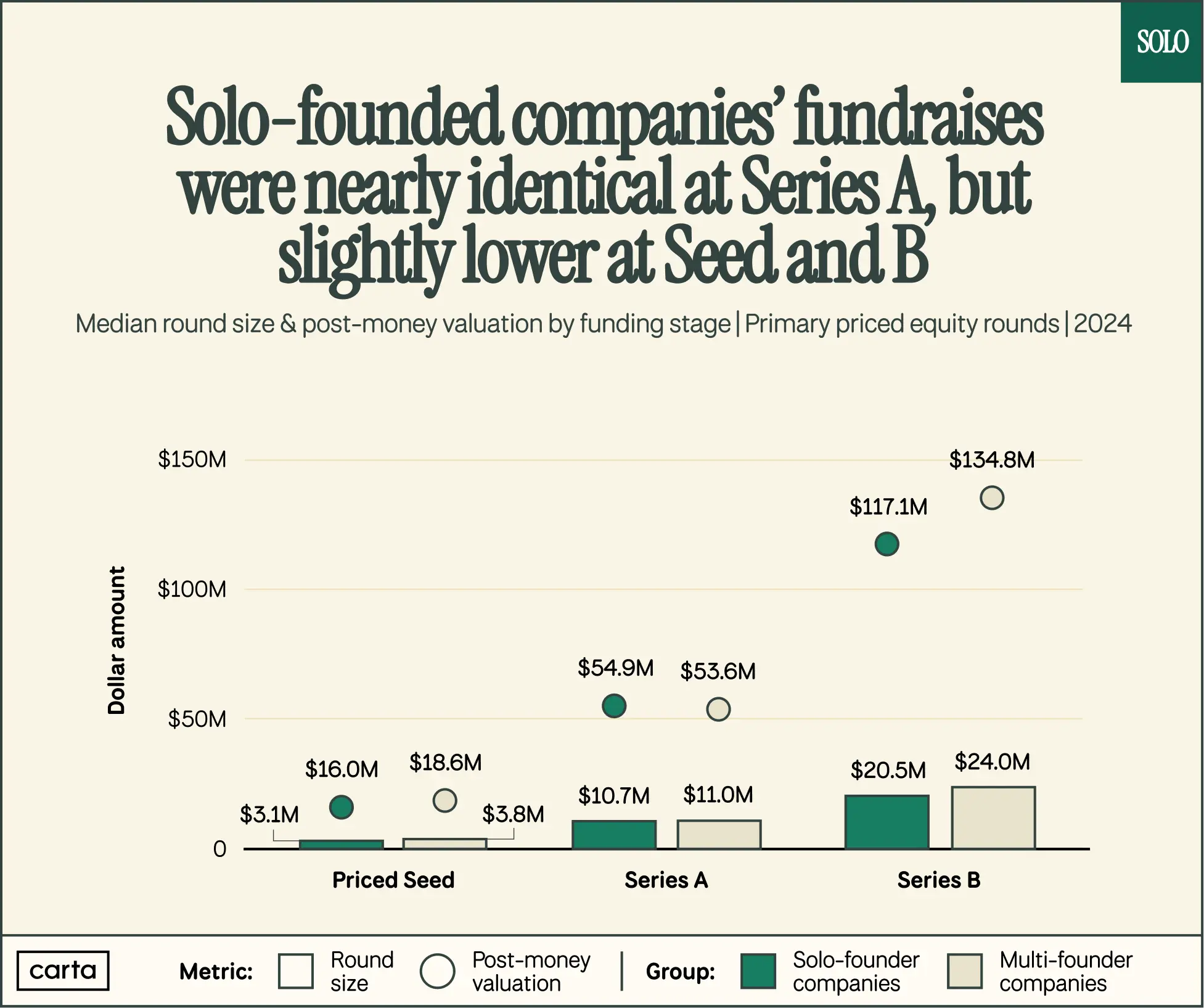

In our Solo Founders Annual Report, Series A medians were nearly identical at $54.9M vs $53.6M, with only slightly lower numbers at Seed and Series B.

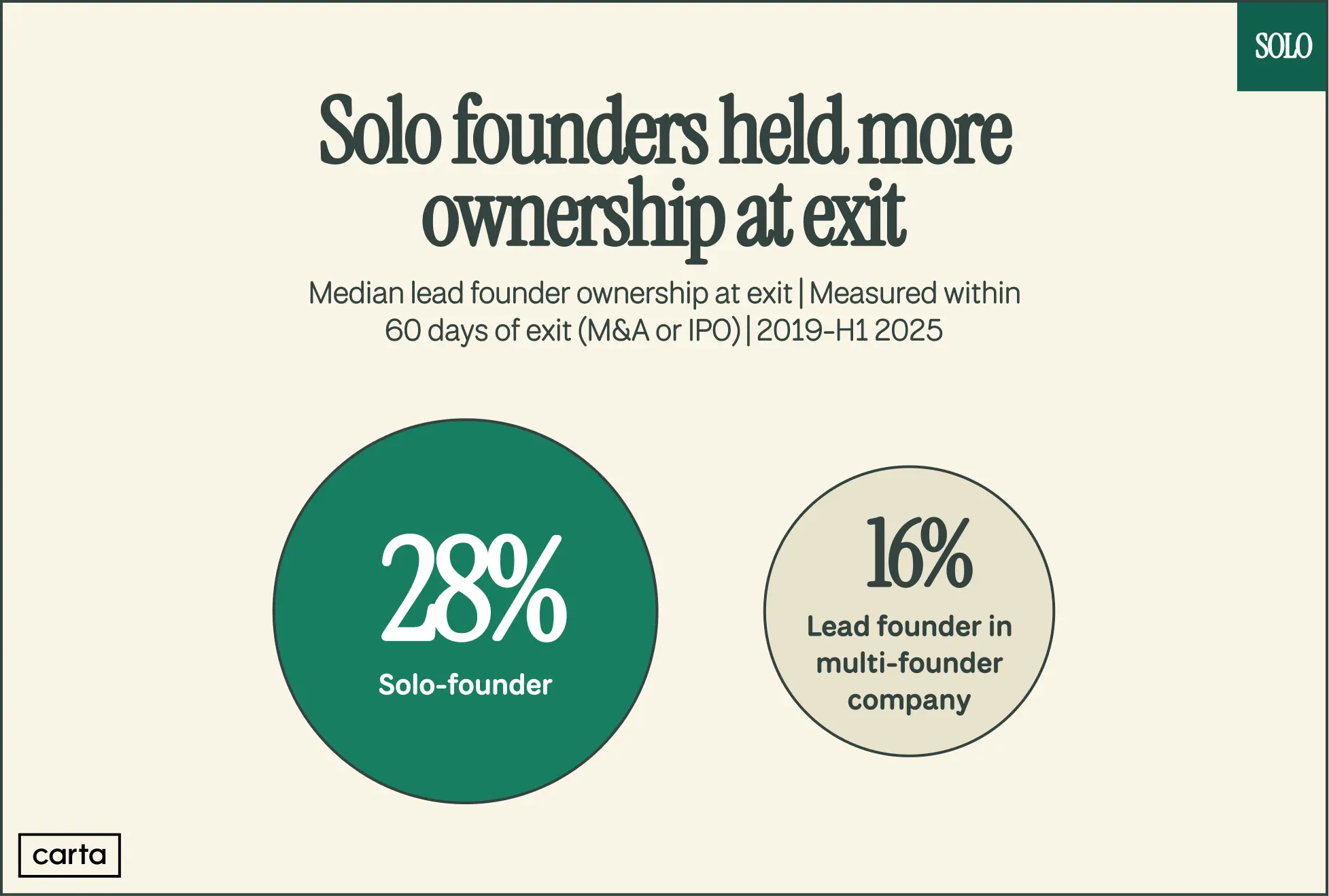

Second, solo founders hold significantly more personal ownership at exit.

Solo founders held 75% more personal ownership at exit than lead founders of multi-founder teams.

Comparable funding along the way. Much more take-home at the end.

The new default

Stripe's insights describe a coherent kind of company: AI-native, B2B SaaS, globally distributed at launch, retention-heavy.

That kind of company has always existed. What’s new is that solo founding is now one of the most natural ways to start it.

The old question was whether solo founders could keep up.

In 2026, the better question might be whether certain companies are now better built solo.

Our answer: solo by default. Consider co-founders only if you have an undeniably outstanding partner.

Additional resources

Ben Cera on the Solo Founders Podcast

Michael Grinich on the Solo Founders Podcast

Paul Klein IV on the Solo Founders Podcast