Fundraising as a Solo Founder: The Data Proves You Won't Pay a "Solo Tax"

For decades, solo founders have faced a hard reality in fundraising: most investors simply wouldn't back them. As Paul Klein IV from Browserbase puts it: "In the past, a key reason not to be a solo founder was the belief that investors wouldn't back you." If you wanted to raise venture capital, the advice was to find a co-founder first.

The data tells an entirely different story.

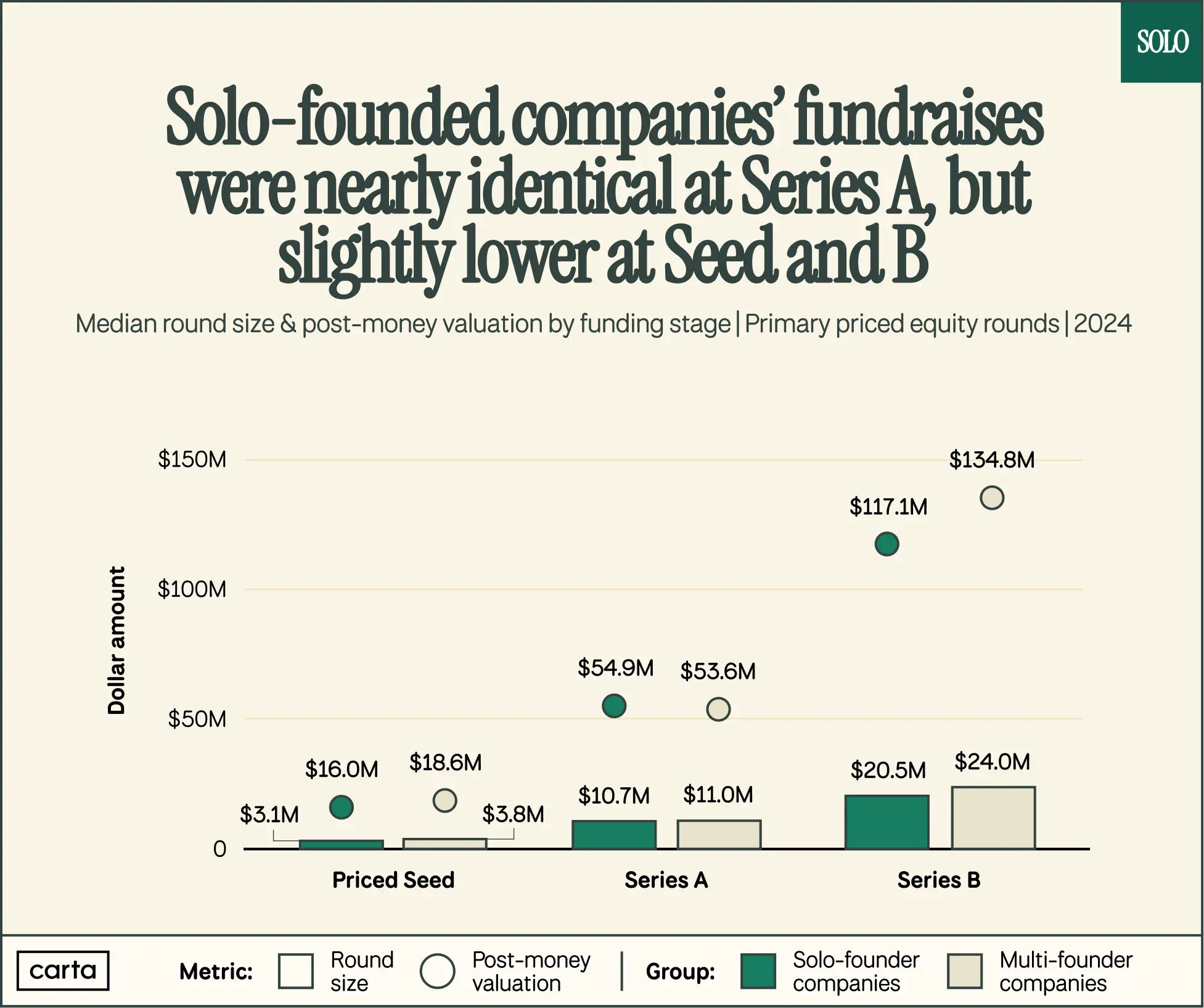

In our report featuring exclusive data from Carta, solo founders are raising substantial amounts of capital on remarkably similar terms to companies with co-founders. Valuations, dilution, and round sizes are nearly identical from Priced Seed to Series B. It turns out, the "solo founder penalty" that conventional wisdom promised barely exists.

This isn't about a handful of exceptional solo founders breaking through. It's a market-wide pattern that suggests fundraising is shaped more by business fundamentals and market dynamics than founding team structure.

The Myth of the Solo Founder Discount

Charles Hudson from Precursor Ventures shares how he actually evaluates solo founders: "My preference is two deeply connected, tightly coupled co-founders who have a lot of trust and previous experience. Of course, even those teams can break up and blow up, but that's the platonic ideal. The second best thing, and the third isn't even close, is a really talented solo founder."

That ranking matters. It's not solo founders versus everyone else, it's solo founders as a close second to the ideal scenario, with mismatched co-founding teams trailing far behind. And when we look at the actual numbers, that second-place position doesn't come with a discounted price tag.

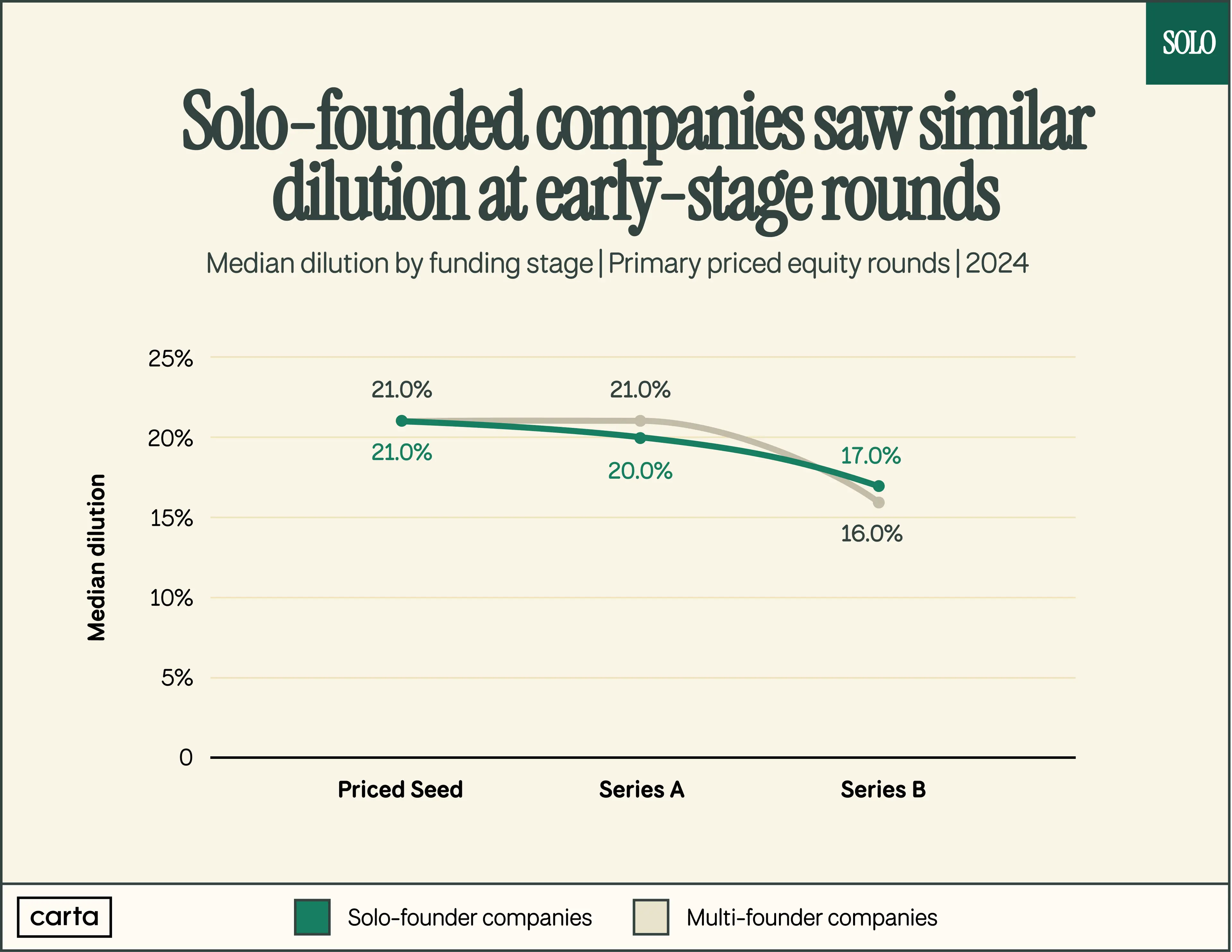

In 2024, solo- and multi-founder companies experienced nearly identical dilution across early funding stages. As Peter Walker from Carta observes: "This tells me that when a solo founder can convince a VC they are a great investment, they don't pay a tax. The VC doesn't demand more equity to counter the perceived risk of a solo founder."

The Pre-Seed Pattern: Why Solo Founders Skip Ahead

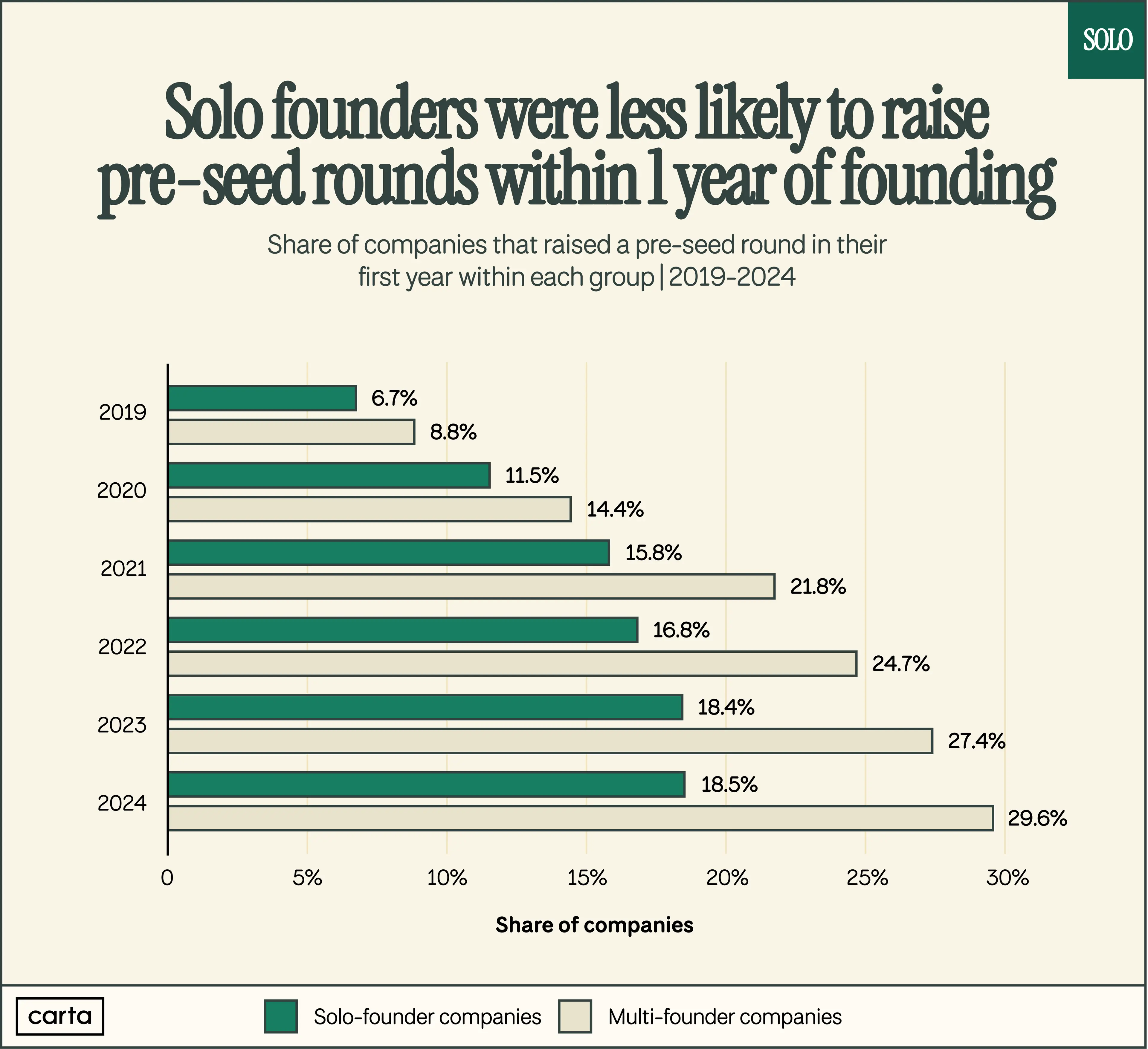

One surprising finding: solo-founded companies were less likely to raise a pre-seed round within their first year compared with companies with co-founders. But before interpreting that as a disadvantage, consider the flip side — solo founders often raise their first priced equity round sooner.

Several factors could explain this pattern. Some solo founders may use their lower burn rate to build more traction before fundraising. With no co-founder salaries to pay, they can tinker, pivot, and experiment longer without needing external capital. When they do raise, they're often further along, which may explain why they skip pre-seeds entirely and move straight to pricing equity.

- Peter Walker

This pattern aligns with what Paul Klein IV from Browserbase discovered: "As a solo founder fundraising, I think you get more bullets. I raised a pre-seed that I probably didn't need and then raised a seed round four months later. Because I'm a solo founder, I have more equity. That gives me a great opportunity to bring more people onto my cap table and give them an early markup."

The Series A Equalizer

At seed stage, investors are mostly evaluating the founding team. A mild bias against solo founders might exist, pulling median valuations slightly lower. But something interesting happens by Series A: the gap essentially disappears.

By Series A, the focus shifts to the business and broader team, so whether there's one founder or several has far less influence on valuation. The product speaks for itself. The numbers speak for themselves. The business performance becomes the evaluation criteria, not the headcount of the founding team.

Charles Hudson confirms this dynamic:

This suggests a strategic implication: solo founders who can bootstrap or stretch early capital to reach Series A metrics may effectively bypass whatever early-stage skepticism exists.

Angels vs VCs: Where Solo Founders Should Start

Founder anecdotes reveal a surprising difference between investor types. Angels and VCs approach solo founders from fundamentally different starting points.

Niels Hoven from Mentava experienced this firsthand:

Angels look for reasons to say "yes." VCs look for reasons to say "no." For solo founders building conviction and early momentum, that distinction can be decisive.

The Compounding Equity Advantage

Here's where the math gets interesting. Solo founders hold substantially more ownership than lead founders in multi-founder companies at every stage. By Series B, solo founders hold a roughly 50% larger personal stake, assuming comparable valuation and dilution levels.

This creates a powerful dynamic where solo founders can be less valuation-sensitive because they're starting with effectively double the equity of their co-founded peers.

- Anonymous founder

When you have more to work with, you can afford to prioritize partner quality over valuation optimization.

What This Means for Solo Founders Raising Now

The data suggests several strategic takeaways for solo founders approaching fundraising:

Don't apologize or mention being solo unprompted. If it was an intentional decision, you shouldn't have to qualify or explain it — and definitely don't until asked. Hudson warns against giving wishy-washy answers about potentially adding a co-founder: "Just say: 'No, it's going to be me. We're building a team, and I'm not looking for a co-founder.'"

Start with angels. The difference in attitude between angels and early-stage funds is stark. Build early momentum with investors who are looking for reasons to believe.

Have a clear hiring plan. Investors will ask how you'll use your extra equity. Be ready to explain how you'll build a world-class team.

Use your equity advantage strategically. You have more bullets. Use them to attract the best partners, the best early employees, and the best investors — even if it means slightly more dilution in exchange for dramatically better support.

The Shifting Perception

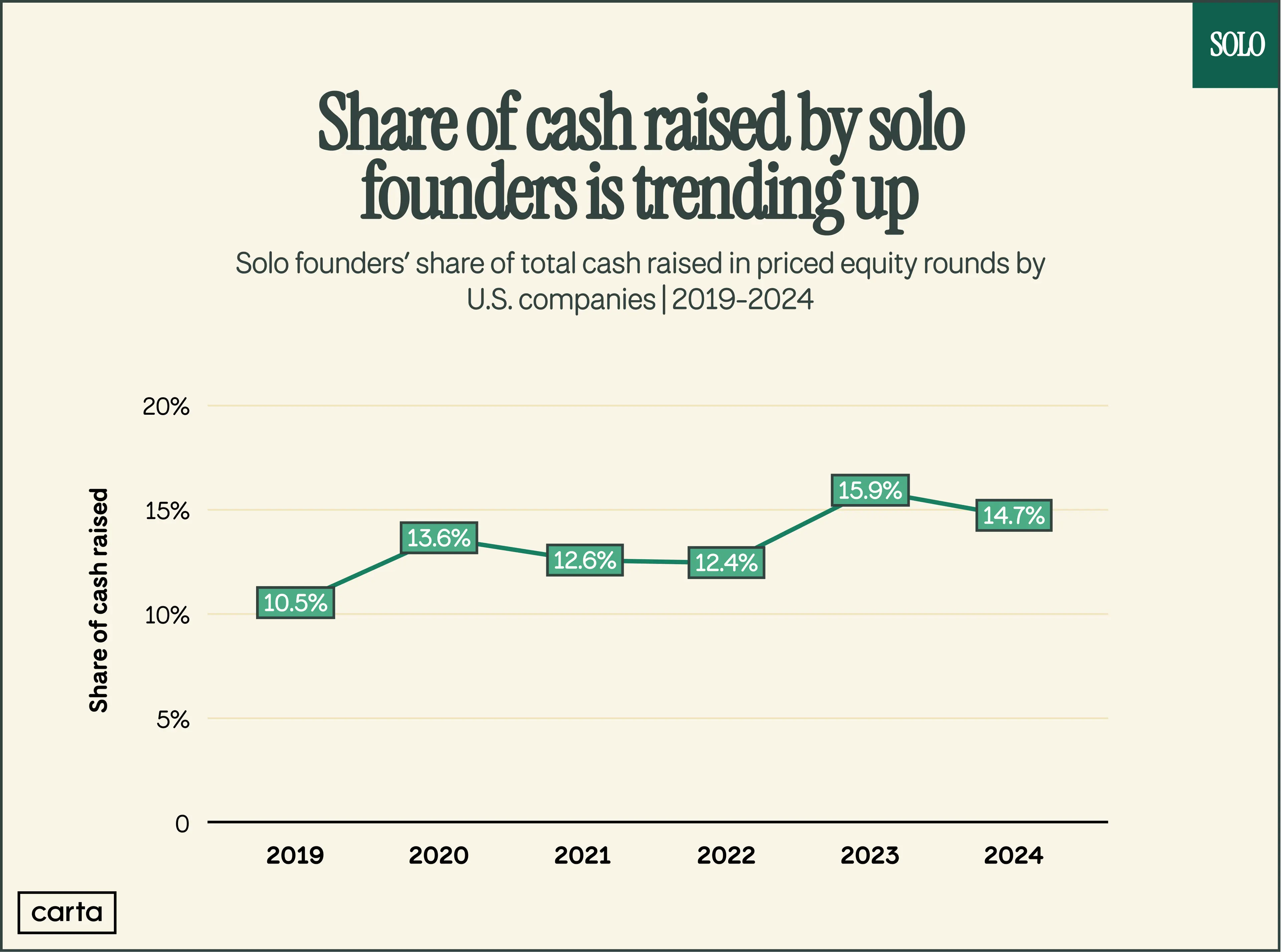

The share of cash raised by solo-founder companies has trended upward over the past several years, from around 10% in 2019 to the mid-teens more recently. Ann Miura-Ko from Floodgate attributes this partly to "investors getting more comfortable after seeing more solo founders succeed."

We're not at parity yet. Solo founders still represent a smaller share of total fundraising than their proportion of new companies would suggest. But the direction is clear, and the penalties are far smaller than conventional wisdom claims.

The old playbook said you needed a co-founder to be taken seriously by investors. The data says otherwise. What matters is the business you're building, the traction you're generating, and the conviction you're creating.

The solo founder penalty is a myth. The data proves it.

This is the second in a series covering the State of Solo Founding report. Read the first chapter on The Rise of Solo Founders or download the full report here. Follow along on Twitter for more insights from our conversations with top solo founders.